Gen Z Consumers Start to Shape Indian Credit Market as They Become Increasingly Credit Active

{kind=link}

- Nearly 9 million Gen Z Indian consumers now credit active

- Two-wheeler loans are the most popular credit product among Gen Z, followed by consumption products such as consumer durables and credit cards

- Credit-active Gen Z consumers more likely to be in near prime and prime risk bands than wider population

Mumbai, Feb. 5, 2020 – Newly released research by TransUnion shows that India’s Generation Z consumers—those born in or after 1995—are becoming increasingly credit-active and are helping fuel the growth of the consumer credit market.

The TransUnion study explored the credit activity of Generation Z consumers (also known as Gen Z) in emerging credit markets including India, Colombia and South Africa, as well as established consumer credit markets including Canada, Hong Kong and the United States. The study explored the depersonalized credit data of Gen Z consumers globally as of Q2 2019 to understand their credit behaviors by country, specifically observing originations, account preferences and balances.

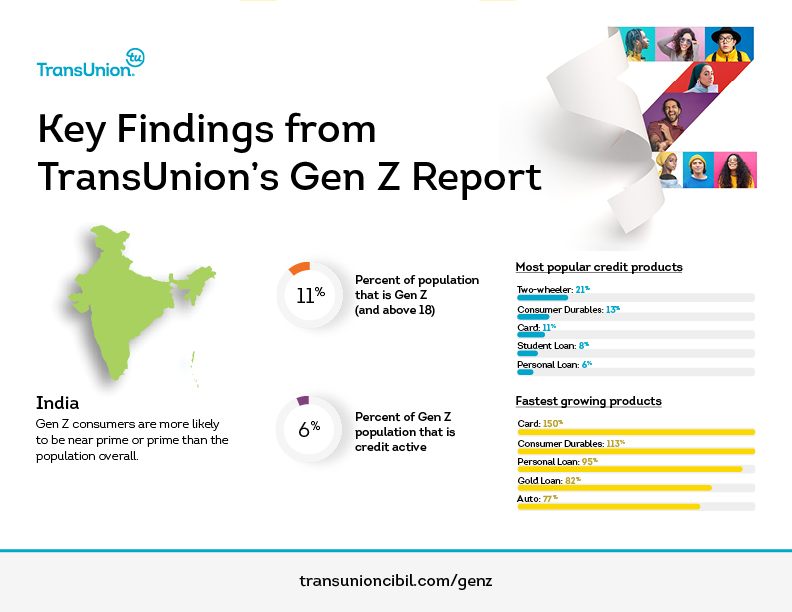

The percentage of the Indian population that was classed as Gen Z, ranging from age 0-24 as of Q2 2019, was 44%, representing more than 609 million people. The percentage of the population that was Gen Z and over 18, and thus eligible to apply for credit, was 11%, almost 147 million people. The TransUnion study revealed that only 6% of this eligible group were credit active in Q2 2019, nearly 9 million people.

Although India had the smallest percentage of credit active Gen Z consumers of all the countries studied, in a country as populous as India, 6% represents nearly 9 million consumers. Even among older Indian generations, credit participation is relatively low, as just 10% of the total adult population is credit active.

“Gen Z is the first generation of digital natives, and they have come to expect a seamless consumer experience across all walks of life – including how they access, use and manage credit,” said Abhay Kelkar, vice president of research and consulting for TransUnion CIBIL. “Our belief is that the desire for credit among this generation is significant and growing at a faster pace than any other generation. As well, the way they apply for and use credit will likely generate an even greater level of demand. Our study shows it is critical for lenders to have the ability to make more informed decisions on prospective customers, including those who are new to credit and have limited or no formal credit histories, and earn their trust as well as their business.”

Gen Z Consumer Credit Usage

The majority (80%) of Indian Gen Z consumers who are credit-active only have one open credit product. The most commonly held products are two-wheeler loans (21%), consumer durables loans (13%), and credit cards (11%).

The percentage of credit-active consumers with two-wheeler loans is higher among Gen Z consumers than any other generation. In comparison, the percentage of credit-active Millennials (consumers born between 1980 and 1994) with two-wheeler loans is less than half that of Gen Z at just 10%, and for Gen X (consumers born between 1965 and 1979) the figure is even smaller at 6%.

Kelkar observed: “The popularity of two-wheeler loans among Gen Z consumers in India is a reflection of where this generation is in its career earnings and wider credit journey. For most, they are unable to afford a car, and having a motorbike or scooter is a convenient and often necessary way to get to work.”

Consumer durables loans are usually used by the broader population to finance large ticket purchases. However, as the second most popular consumer credit product among Gen Z consumers, they are most likely to be used to buy a smartphone, personal computer or laptop, or even a television, rather than household appliances like refrigerators or washing machines often preferred by older generations.

For Gen Z, credit card participation is growing, but remains low compared to the wider national average. Looking at the entire adult population in India, overall credit card penetration among credit-active consumers is 21%. While 11% of Indian Gen Z credit-active consumers with a credit card is fairly low compared to other countries in the study (Hong Kong and Canada have rates above 90%), it’s encouraging for lenders that the youngest generation is adopting cards early in their credit life.

Most Popular Credit Products Among Gen Z Consumers

(Percentage of Credit-Active Consumers with Each Product Type)

|

Two-wheeler |

Consumer Durables |

Credit Card |

Student Loan |

Personal Loan |

|

21% |

13% |

11% |

8% |

6% |

For Indian Gen Z consumers, originations (the rate at which new accounts are being opened) are growing fastest in the consumption lending categories. Looking at year-over-year growth in originations in Q2 2019, credit cards grew 150%, consumer durables 113%, and personal loans 95%. Personal loans and credit cards are often used to finance living expenses and make smaller-ticket purchases. In the personal loans space especially, the prevalence of non-banking financial companies (NBFCs) and the rapid growth of FinTech lenders has accelerated the availability and ease of application for this particular credit product.

Risk Distribution

A common myth is that all (or at least the vast majority) of Gen Z consumers are in the subprime credit tier because they have fewer open credit products and don’t have long histories of positive credit repayment. There is also the assumption that new-to-credit consumers receive lower limits, driving higher utilization and negatively impacting their credit scores.

However, the TransUnion global study found that in all markets, the majority of Gen Z consumers are not subprime, and India was no exception.

Compared to the overall credit active population in India, Gen Z consumers are more likely to be near prime or prime, and overall just over half (51%) have credit scores in the prime and above risk tiers.

Risk Tiers: Gen Z vs. Total Credit Active Population

|

Credit Tier |

% of Gen Z Consumers |

% Total Credit Active India Population |

|

Super prime |

2% |

5% |

|

Prime plus |

9% |

15% |

|

Prime |

40% |

32% |

|

Near prime |

27% |

23% |

|

Subprime |

22% |

25% |

*TransUnion CIBIL Credit Vision (CV) score tiers: subprime = 300-680, near prime = 681-730, prime = 731-770, prime plus = 771-790, and super prime = 791-900. Higher scores are indicative of lower risk. Grouped together, below prime segments constitute a CV score of ≤730 and prime or above a CV score of ≥731.

International Comparisons

According to the study, there is a relatively large divide in how Gen Z approaches credit in emerging versus established credit markets. While in most established markets more than half of Gen Z are already credit active, the percentages drop precipitously for emerging markets.

Percentage of Gen Z Population (over 18) that is Credit Active with Traditional Credit Products

|

Canada |

Colombia |

Hong Kong |

India |

South Africa |

United States |

|

63% |

19% |

49% |

6% |

28% |

66% |

**For this study, consumers are considered credit-active when they open a traditional lending product such as a credit card, auto loan, mortgage, personal loan, or student loan.

“In emerging markets, lenders may be more conservative with extending traditional credit products to Gen Z, as those consumers may not yet have the credit histories and track records those lenders use to assess and manage risk,” said Kelkar. “We have seen that the use of expanded data sets and advanced analytic techniques can help lenders better understand the risk profiles of these younger borrowers and identify ways to engage them in a mutually profitable manner. Lenders that incorporate trended credit and alternative data can gain a better understanding of the specific risk profiles of Gen Z and as a result, are broadly able to provide more consumers with access to traditional credit products. The ability to ensure each consumer is reliably and safely represented in the marketplace will be critical for companies that want to engage this increasingly important market segment.”

About TransUnion CIBIL

India’s pioneer information and insights company, TransUnion CIBIL makes trust possible in the modern economy. We do this by providing a comprehensive picture of each person so they can be reliably and safely represented in the marketplace. As a result, businesses and consumers can transact with confidence and achieve great things. We call this Information for Good. ® TransUnion CIBIL provides solutions that help create economic opportunity, great experiences and personal empowerment for millions of people in India. We serve the financial sector as well as MSMEs, corporate and individual consumers. Our customers in India include banks, financial institutions, NBFCs, housing finance companies, microfinance companies and insurance firms.